Crypto

3 minutes

Stablecoins explained: what UK business owners need to know

Move money across borders faster, cut conversion costs and settle payments in minutes – all with a pound stable digital currency backed by regulated frameworks.

Ahmed Zifzaf

Head of Crypto Partnerships

Ahmed Zifzaf leads crypto partnerships at Worldpay, now Global Payments, spanning stablecoin settlement, programmable treasury and on-chain payment infrastructure. He previously advised Fortune 500 firms at McKinsey and holds an MBA from Stanford GSB.

Key points

- Stablecoin supply grew 59% from 2024 to 2025 (Messari), and 58% of European financial firms surveyed in 2025 were already using stablecoins or planned to – a trend driven in part by MiCA bringing regulatory clarity to euro-pegged stablecoins.

- Businesses with cross-border payment needs can now operate within defined legal frameworks across both the EU (MiCA) and the U.S. (GENIUS Act), with the FCA actively developing its own UK stablecoin framework.

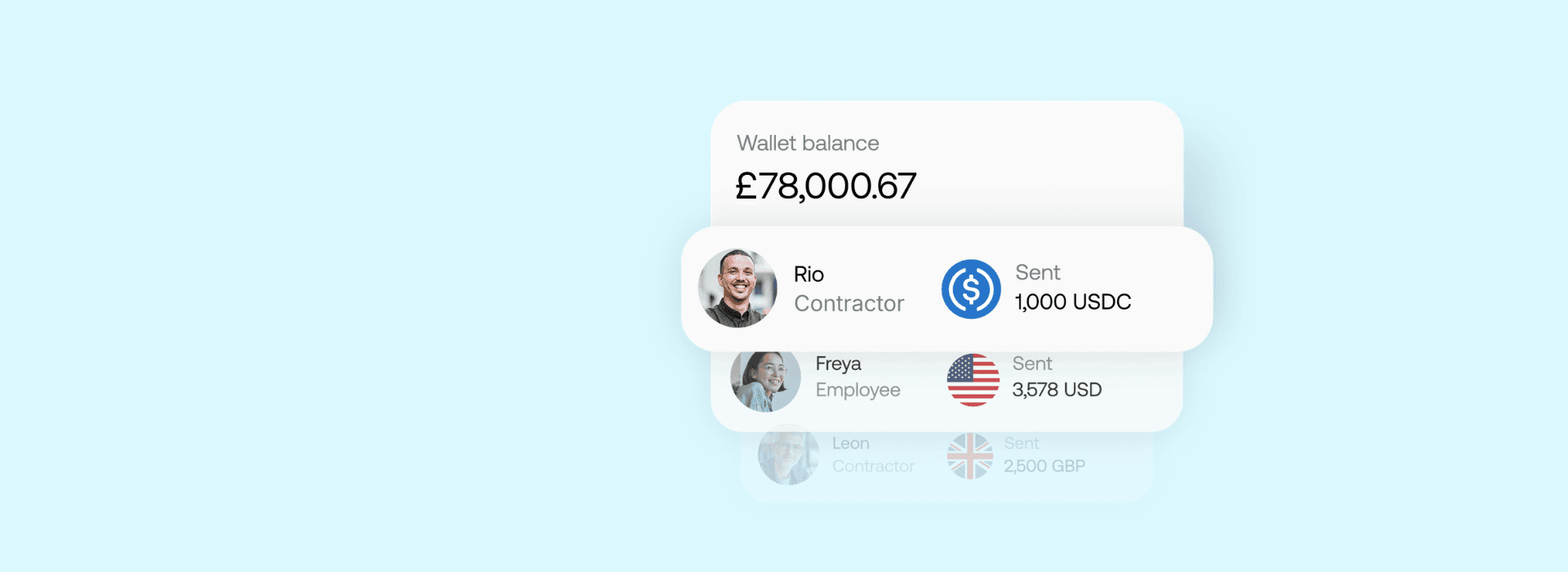

- Worldpay supports stablecoin settlement in USDC and USDG, with EU stablecoin settlement available through our Zerohash partnership – covering the U.S. and EU corridors most relevant to UK businesses trading internationally.

If your business pays EU suppliers, works with U.S. clients or collects revenue from international markets, you've seen the friction: slow settlement, conversion fees, local banking infrastructure that doesn't always cooperate. Stablecoins settle in minutes on a blockchain network – no correspondent banks, no layered charges. With regulatory frameworks now active across the EU and U.S., they're worth understanding. Here's a plain-English guide.

What are stablecoins, and how do they work?

A stablecoin combines the value stability of a fiat currency with the speed and reach of blockchain technology. When you send a stablecoin payment, it settles directly on a blockchain network – often in minutes – without passing through correspondent banks or local clearing infrastructure.

The most widely used stablecoins are dollar-backed: USDC (issued by Circle), USDT (issued by Tether), and USDG (issued by Paxos). Euro-pegged stablecoins are also growing: EURC (Circle) and EURS (Stasis) are currently the largest by market cap in the eurozone, a development driven partly by the EU's MiCA regulatory framework coming into force.

It's worth understanding what stablecoins are not. They're not the same as Bitcoin or other volatile crypto assets – the entire point is that the value stays fixed. They're also different from central bank digital currencies (CBDCs), which are issued by governments, and from deposit tokens, which are digital representations of money held in a commercial bank account.

59% |

|---|

Growth in stablecoin supply from 2024 to 2025 (Messari, State of Stablecoins 2025) |

Why are businesses using them?

For businesses that move money across borders, stablecoins can address three friction points in traditional payment infrastructure.

Speed. Because stablecoins don't rely on correspondent banks, they aren't dependent on local clearing infrastructure. International transfers that take two to five business days through traditional banking can settle in minutes. For UK businesses paying EU suppliers, U.S. contractors or partners in markets with fragmented banking systems, that speed difference is practical, not theoretical.

Stability. Businesses operating in markets with volatile local currencies can hold revenue in a dollar-pegged stablecoin rather than converting it immediately. This reduces exposure to currency swings between the time a transaction completes and funds are accessed – relevant for UK businesses with exposure to emerging market revenues.

Lower conversion costs. Cross-border payments typically involve multiple currency conversions, each carrying fees. Stablecoins let you move value across borders in a single asset, reducing the layering of conversion costs and wire fees. The EU corridor in particular is becoming more accessible as euro-pegged stablecoins grow under MiCA.

What's happening with regulation – and what it means for UK businesses

The regulatory picture for stablecoins has changed considerably in the past 18 months. Across the EU, U.S. and Asia-Pacific, frameworks that were previously absent or unclear are now in place.

In the EU: The Markets in Crypto-Assets (MiCA) regulation is now largely in force. It covers the issuance of stablecoins, licensing requirements for issuers and the supervision of crypto-asset service providers. The practical effect is already visible – euro-pegged stablecoins have grown substantially since MiCA took hold, with Circle's EURC leading by market cap. For UK businesses trading with EU counterparties, this matters: Stablecoin settlement across the EU corridor is becoming more structurally viable.

In the U.S.: The GENIUS Act, signed in 2025, established the first federal framework for stablecoin payments. It defines who can issue a stablecoin, what backing standards apply and how stablecoins can be used. For UK businesses with U.S. customers or suppliers, this regulatory confidence on the U.S. side increases the practicality of dollar-stablecoin transactions.

In the UK: The UK is moving towards a full stablecoin regime, with detailed rules from the FCA and Bank of England expected in 2026 and implementation by 2027. The framework splits oversight between regulators and focuses on making stablecoins safe for everyday payments while supporting innovation. Key details are still being refined to balance strict safeguards with making the UK competitive.

Across Europe, 58% of respondents to a Fireblocks survey in 2025 said they were already using stablecoins or planned to use them (Fireblocks, State of Stablecoins: 2025).

What are the risks to know about?

Stablecoins offer genuine benefits for some business use cases – but they also carry risks worth understanding before adopting them.

Depeg risk. The primary financial risk is the possibility that a stablecoin drops below its pegged value – typically caused by a sudden drop in demand or inadequate collateralisation. Well-backed stablecoins like USDC and USDG maintain 1:1 reserves and are subject to regulatory oversight, which reduces this risk considerably. Smaller or less regulated stablecoins carry higher exposure.

Compliance obligations. The pseudonymous nature of public blockchains creates considerations around anti-money laundering (AML) and counter-financing of terrorism (CFT) compliance. Working with a regulated payment provider helps ensure you meet your obligations under UK regulations.

Not all stablecoins are equal. Issuer quality, reserve backing and regulatory standing vary. Sticking to well-established, regulated stablecoins – and working through a payment processor with stablecoin expertise – limits exposure to the tail risks of the broader market.

Competition from alternatives. Citi's "Stablecoins 2030" report projects base-case stablecoin issuance of $1.9 trillion by 2030. But it also notes that bank token transaction volumes could reach $4 trillion in that period, with bank tokens preferred by many corporates. Stablecoins are one option in an evolving toolkit – not the only one.

Is this the right move for my business?

Stablecoins are most useful for businesses with cross-border payment needs: paying EU or international suppliers, receiving funds from U.S. or overseas customers or operating in markets where local banking infrastructure is slow or fragmented.

If all your transactions are domestic sterling payments through existing rails, the practical benefit is more limited. The infrastructure already works well for that use case.

'Stablecoins are most useful for businesses with cross-border payment needs.'

For businesses that do trade internationally, the question is less whether stablecoins will become a standard part of the payments toolkit and more when and how to integrate them. The regulatory frameworks are in place – in the EU and U.S. at minimum. The technology is proven at scale. And euro-pegged stablecoin options are growing specifically because of the regulatory clarity MiCA has provided.

Worldpay supports stablecoin settlement in USDC and USDG, and offers EU stablecoin settlement through our partnership with Zerohash. We can help you assess whether stablecoin payments fit your business and what integration looks like in practice.

Stablecoin FAQ

What is a stablecoin in simple terms?

Are stablecoins legal in the UK?

Can a small business accept stablecoin payments?

What's the difference between a stablecoin and cryptocurrency?

How does MiCA affect stablecoin payments for UK businesses?

Related insights